Blair Hull is a legend of Wall Street and a former professional blackjack player. He was named by Worth magazine as one of Wall Street’s 25 smartest players and by Forbes magazine as one of the most successful traders of the last 40 years.

Today, Hull operates a number of ventures including an ETF that attempts to time the S&P 500 through a mix of 12 technical and fundamental indicators. In this article, we will look at the idea behind Blair Hull’s strategy and the 12 indicators he uses.

Blair Hull ETF

Back in August of 2015, the S&P 500 was trading 7.5% lower than its recent highs – a modest correction but still a significant one for most investors.

At the same time, famed trader, investor and gambler Blair Hull and his Hull Tactical US ETF (HTUS) was down only 1.4%, with the bulk of its holdings sitting on the sidelines in cash. His ETF had once again dodged a sharp drawdown thanks to the multi-factor model he uses to time the market.

Academic Theory

Hull’s ETF is built around research that suggests it’s possible to use a range of technical and macroeconomic variables to predict future returns of the overall stock market over the medium term.

What is even more interesting is the fact that the variables are all straightforward and chosen because of academic research that supports market prediction. Hull incorporates widely known variables including the PE ratio, CPI, moving averages and even seasonality, to help develop his market timing model.

While the indicators do not amount to much on their own, it is when they are combined together that the real magic happens with regard to estimating future returns.

Hull’s research suggests that depending on how positive (or negative) those future returns appear, gives him the opportunity to optimally position his portfolio.

He is then able to shift between being fully invested, in cash, or short the market depending on the output of the model. The goal of the model is to outperform the market and in the process significantly reduce drawdowns.

Multi-Factor Model

In the paper A Slightly Predictable Stock Market, Blair Hull reveals the method he uses to construct his model. He weighs 12 factors to determine predicted future returns and then buys (or sells) S&P 500 E-Mini futures contracts, in direct proportion to his perceived edge.

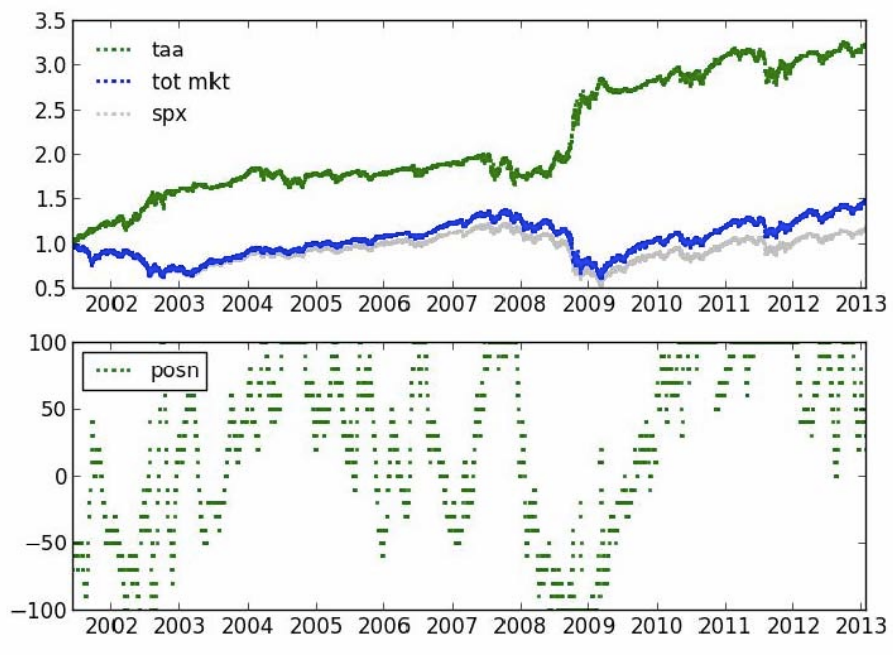

The simulated results (shown below) were able to achieve a 19% annual return with a Sharpe ratio of 1.08 between June 2001 through to January 2013 (green line). While over the same period, a buy and hold strategy (blue line) would have returned 3.1% with a Sharpe ratio of 0.24.

As mentioned, the interesting element of this strategy is that Hull incorporates variables in his analysis that are based heavily on academic research. He initially had a list of 18 individual factors that had been shown in academic studies to lead to out-performance.

He then took a subset of those variables and using regression analysis, quadratic programming and machine learning weighed them every two weeks, according to a proprietary algorithm.

Examining The Factors

All of the variables Hull uses to make his prediction must first have a common sense relationship to stock market returns. They then must have a proven edge documented in academic studies.

Here’s the list of 12 of Hull’s key factors:

All of these indicators have been shown in the literature as being predictive or at least slightly predictive of market returns.

The PE ratio, for example, is mentioned as being predictive of up to 40% of total market returns. Relative strength, meanwhile, has been written about by Meb Faber.

The seasonal strategy of selling in May has also been shown to be a statistically significant pattern and the Baltic Dry Index has been shown to be a leading indicator of future economic growth.

Meanwhile, the dollar has been shown to have a negative correlation with the S&P 500 and increased durable goods orders and shipments have been shown to indicate peaks in the business cycle (thereby being a bearish indicator).

All of the indicators when combined can produce a powerful model for market timing.

Using Variables In Your Own Trading

There are many examples of quantitative and system traders using factors like these in their trading strategies.

There’s been research into the power of momentum indicators, PE ratios, volume, relative strength, the 200-period moving average as well as seasonality.

However, Hull is able to not only use technical factors but also fundamental and economic data to build a robust tactical asset allocation model that weighs each factor.

He has managed to effectively create a market filter to time the market and allocate capital according to his prediction of what the market is likely to do in the medium term.

If the model indicates a bullish or bearish bias, Hull is able to position himself anywhere between 100% short to 200% long with the use of S&P 500 futures contracts.

Note that ordinary investors can also use ETFs if they do not have access to futures markets.

Hull Tactical US ETF (HTUS)

To date, Hull’s ETF has achieved an average annual return of 5.96%, slightly higher than a 60/40 S&P 500 / Citigroup 3-Month Treasury Bill portfolio – its benchmark.

The great thing about Blair Hull’s trading strategy is that he discloses the indicators he uses and discusses his methodology in the white paper.

Not only that, but investors can buy into his model directly via the ETF and even get daily trading signals of the strategy straight from Blair Hull’s Tactical Fund’s website.

As of the 17th July 2017, the website showed the strategy had an allocation of 80% cash and 20% to the S&P 500.

Data Sources

As mentioned, it should be possible for most investors to access the same data sources used by Blair Hull. Market PE ratios are widely available while CAPE can be found on the website of Professor Shiller. Many economic indicators can also be found on excellent websites like FRED, Quandl and EconoMagic.

As well, Norgate data provides a number of economic indicators that can be accessed directly through back-testing platforms like Amibroker.

For example:

- Durable Goods New Orders – Symbol #DURSA

- US Consumer Price Index – Symbol #CPISA

- US Dollar Index – Symbol $USDX

- VIX Index – Symbol $VIX

- US Ten-Year Yield – Symbol %TNX

In future articles I will use some of these time series to create market timing indicators and back-test individual trading systems.