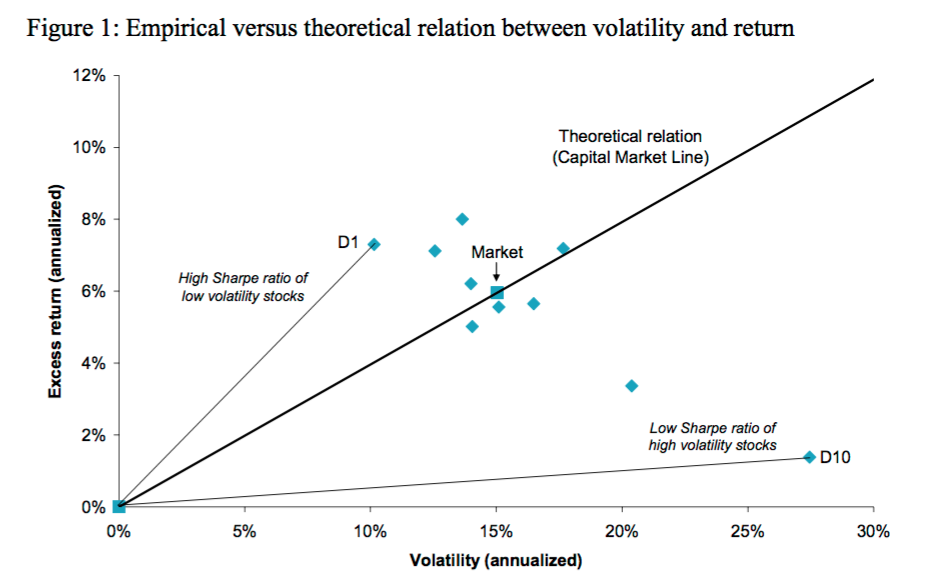

There is substantial evidence that high volatility stocks earn abnormally low returns while low volatility stocks are lower risk and thus a better choice for investors.

In this article, I take a look at the facts and present a number of strategies. The best of which is to buy low volatility stocks in low volatility environments.

The Volatility Effect In Stocks

On the website Quantpedia, an interesting strategy is shown that goes long low volatility stocks.

The strategy involves ranking stocks on the past three year volatility of weekly returns and then going long each month the lowest ranked (lowest volatility) firms. The strategy was shown to outperform high volatility stocks by as much as 12% per annum.

The results seem fairly robust and similar results have been reported in other academic research.

After reading such papers I wondered if there would be any way to improve on these results and what would be the effect of including an overall market volatility filter i.e. by using the VIX.

We will now consider a handful of very simple strategies that attempt to harness the volatility effect in stocks and produce the backtest results of those ideas.

Low Volatility Stocks With Trailing Stop

The idea of this simple strategy is to rank S&P 1500 stocks by volatility and pick the 25 least volatile stocks over the last 252 trading days then sell by 20% trailing stop.

In this way, we hope to buy less volatile companies and ride them on a new upward trend.

Several different methods for measuring volatility were considered but I settled on ATRP, which is simply the average true range normalised for price.

Thus, stocks with smaller ATRP values are picked first ahead of more volatile tickers.

So, for this first backtest, we will buy low volatility stocks from the S&P 1500 universe (including delisted tickers). We will use transaction costs of $0.01 per share and we will include a 30-day turnover minimum of $500,000 as a liquidity filter.

The portfolio can hold a maximum of 25 positions and capital will be split equally between each one.

Furthermore, all trades will be executed on the next day open.

Using Amibroker and historical data from Norgate, we recorded the following results and equity curve between 1/2000 – 1/2017:

CAR: 12.71%

MDD: -48.60%

CAR/MDD: 0.26

Win Rate: 52.42%

You can see that for such a simple strategy, the results are pretty good.

They are superior to a buy and hold return on the SPY ETF which was 4.51% (CAR) with a max drawdown of -55.19%.

Low Volatility Stocks In Low Volatility Times *Best*

Next, we have the same strategy rules and settings but we can only buy stocks when the VIX trades under it’s 200-day moving average. When the VIX is trending above it’s 200-day MA we aren’t allowed to buy.

Thus, we are building a portfolio of 25 of the lowest volatility stocks only during low volatility market periods.

CAR: 12.13%

MDD: -26.40%

CAR/MDD: 0.46

Win Rate: 60.43%

As you can see, our annualised return has dropped slightly from the first test but we have almost cut our drawdown in half making these results much better on a risk-adjusted basis. Our win rate is significantly higher too.

Next, we can also compare these results to similar strategies along the same theme.

Low Volatility Stocks In High Volatility Times

In this example, we use the same rules but we can only buy when the VIX is above it’s 200-day moving average. So now we are buying low volatility stocks in high volatility periods:

CAR: 11.98%

MDD: -42.66%

CAR/MDD: 0.28

Win Rate: 51.25%

Here we have got another decent result but it’s not as strong as the two previous tests.

High Volatility Stocks In Low Volatility Times

This time, we will rank the stocks in reverse so we will buy the 25 most volatile stocks but only when the VIX is below it’s 200-day moving average.

To be fair to the highly volatile stocks, exits will now be made by 50% trailing stop instead of 20%.

CAR: 5.98%

MDD: -70.31%

CAR/MDD: 0.09

Win Rate: 33.69%

As you can see, we have recorded a poor result with this combination of rules.

High Volatility Stocks In High Volatility Times

Finally, we can see what happens if we buy the 25 most volatile stocks during the most volatile periods (i.e. when the VIX is above it’s 200-day moving average). Exits are again by 50% trailing stop.

CAR: 2.30%

MDD: -72.45%

CAR/MDD: 0.03

Win Rate: 33.73%

As you can see, this combination gives us the worst result of all!

Conclusions

In this article we investigated an academic paper that talks about the low volatility effect in stocks.

We then constructed various strategies around the same theme.

As you can see from these results, buying low volatility stocks during low volatility market periods appears to be the best strategy according to historical simulations.

So far in 2017 this strategy is up 16.69% with a drawdown of just -2.51%.

When selecting stocks, therefore, investors would be wise to prefer lower volatility stocks according to this analysis. They may also consider shorting high volatility stocks as part of a combined long/short strategy.

Overall, the volatility effect is pretty clear and shows potential for further development.

Simulations and charts from Amibroker. Data from Norgate.

Hi Marwood, can you please share the AFL of this strategy.

Thanks,

Zohan

Sorry I no longer have the code to hand. There is a version of this in our course Expert Trading Strategies. Thanks. https://marwoodresearch.teachable.com/p/marwood-research