It’s a fair assumption that managers will have a better insight into the financial state of the company they’re running than outside investors. A manager will act and make decisions that are based around what they perceive the outlook for that company to be.

It’s also assumed that when a company makes a corporate action, such as a share buyback, a merger, a dividend or an equity issue, as soon as it’s announced, the market factors that into the price to reflect the potential long term impact of the decision.

However, a new paper by Amini and Singal suggests that the information contained in particular corporate actions are in fact not fully incorporated into the price of a stock after they are made known to the public.

The authors suggest that you can even predict the future earnings of a company, based on their prior corporate actions.

Predicting Earnings Following Equity Issues And Buyback Announcements

The study looks specifically at share buybacks and equity issues as they in particular give an insight into the way managers are thinking. For the most part, a share buyback reflects a positive outlook for a company, while an equity issue is generally seen as a negative.

The authors track earnings announcements that immediately follow both of these corporate actions as a way to gauge just how much of the information has been priced in.

Theoretically, corporate announcements should be fully priced into the stock price by the time the earnings data is released. However, results from the study seem to confirm this isn’t always the case.

Key Insights From The Study

The study looked at 15,106 share buyback announcements between 1994 and 2015 and 19,466 equity offerings that were not IPOs between 1970 and 2015.

As it turns out, buying stocks prior to earnings announcements that had recently announced a share buyback showed a persistent positive return.

Furthermore, shorting stocks prior to earnings that had recently announced an equity issue, also showed a persistent positive return.

If you were to buy a stock that had recently announced a share buyback two days prior to an earnings announcement and sold it 30 days later you would have earned a raw return of 3.31% according to results shown in the paper.

Similarly, if you were to short a stock that recently announced an equity issue two days prior to earnings and closed that 30 days later, you would have earned a 1.57% raw return.

The study also shows that a portfolio of long buybacks and short equity issues prior to earnings announcements generated a raw return of 1.74% and a four-factor adjusted return of 4.47%.

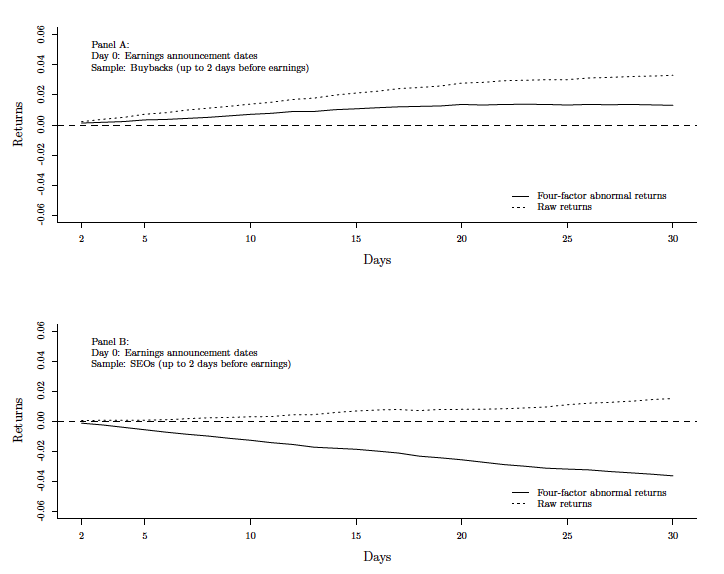

The following two charts are taken from the paper and show the abnormal returns around the earnings date for companies that issues either buyback announcements (top) or equity issues (bottom).

announcement up to 2 days before earnings. Panel B plots the returns around earnings for issuing

firms that priced an equity off ering up to 2 days before earnings. Src: Amini, Shahram and Singal, Vijay, Predictability of Earnings Following Equity Issues and Buyback Announcements (June 9, 2017).

It appears from these charts that returns are significant and persistent although there are some differences between the two types.

Returns following buyback announcements appear to peak at around 15 days after the earnings announcement. Meanwhile, the negative returns following equity issues takes considerably longer to diffuse.

Economic Rationale

The paper points to the fact that share buybacks and equity issues are giving an insight into the potential profitability of the company in the short run.

Theoretically, if a company is going to perform strongly and have excess cash reserves, they would have the ability to buy back shares.

Buying back shares is an effective way for companies to give back value to its shareholders – just like issuing a dividend. It also signifies confidence in the business and may give off a positive signal about the market cycle.

Furthermore, if a company plans to buy back shares it would make sense to do so before a positive earnings announcement. If it delays the buyback until after the announcement the share price is likely to be higher and therefore the buyback operation would be more costly.

Similarly, a company that hasn’t met its profit targets and is in need of a further cash injection would be a candidate for a share issue to raise further capital to fund its operations.

Going into either – a share issue or a buyback – the managers of the company would have a greater understanding about the financial state of the company and its profit potential than outsiders.

This information is telling when it occurs very soon before an earnings announcement and suggests that the information is valuable to outside investors.

As a result, investors can use these types of corporate actions to gain additional insights into how the managers are viewing the outlook for the company and therefore how they can expect future earnings announcements to unfold.

Key Takeaways: How Can Investors Use This Information?

- Look for earnings announcements that follow a recent corporate action.

- If the corporate action is positive like a share buyback, then the stock has the potential to outperform following its earnings announcement. Look to buy.

- A negative corporate action like a equity issue, means that a company will potentially underperform following its earnings announcement. Look to short.

- Websites such as Finviz and RTT News can be used to track earnings and buybacks.

Quantopian & Quantpedia

As well as the research provided by Amini and Singal, there is also some work on this subject done by Seong Lee in Quantopian and the team at Quantpedia.

Looking at the evidence from the same research paper, Seong Lee has constructed an implementation of the buyback part of the strategy and provided the source code which is available for free on Quantopian.

Lee’s analysis looks at the top 2,000 most liquid US stocks and goes long any stock that has announced a buyback 0-15 days before an earnings announcement. Lee finds that performance is strongest when holding for 5-15 days after the buyback announcement.

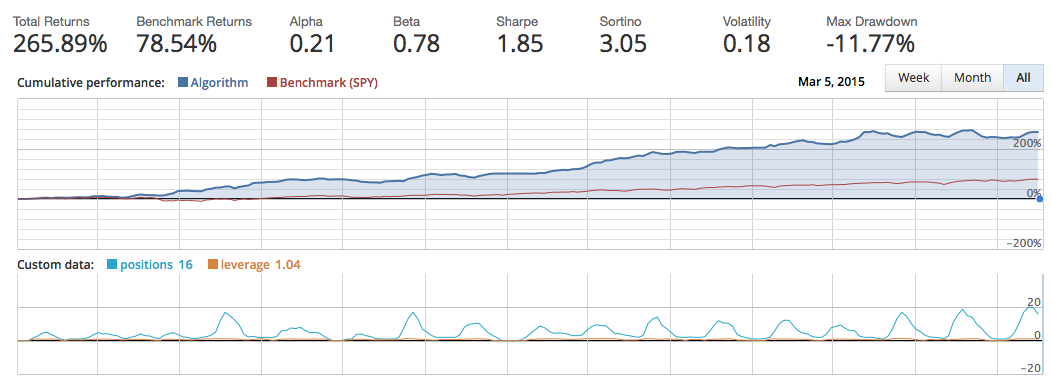

I amended Lee’s strategy to look for buybacks within 5 days of earnings and use a holding period of 15 days not 25. I produced the following equity curve in Quantopian between January 2011 – March 2015:

Thanks for the post on this Joe. I’ve always wondered to what extent corporate actions like this had an impact on share price. Appreciate you sharing this research that begins to quantify it!

Awesome article! Thanks for this.

No worries, thanks for the comment

Great article! I was wondering how you got the information on corporate action dates? What do you use for your data sources? Thanks!