Sluggish growth and anaemic inflation has seen global commodity prices fall steadily in value since 2008. Because of this, and with stock markets reaching new record highs in 2017, commodity trading has gone out of fashion.

Yet in the past, commodities have provided a good source of returns for both investors and active traders. Furthermore, there is evidence to suggest that commodities can provide less volatile returns than some stocks.

Investing In Commodity Futures

Most traders and investors are familiar with equities and bonds, however far fewer have used commodity futures as an investment vehicle.

Over the long term, US equities have returned roughly 10% per year as well as being relatively consistent and relatively safe.

When compared with other asset classes over very long periods, the general consensus is that equities have been able to outperform by some margin.

However, a paper by Gary Gorton and K. Geert Rouwenhorst suggests that investors should consider adding a combination of commodity futures to their portfolios, to not only generate solid long term returns, but to also act as a hedge when the stock market is performing poorly.

Futures Contracts

If you are unsure, a futures contract is a financial instrument known as a derivative, as it gains its value from something else. For example the price of a crude oil futures contract is based on the expected future spot price of a barrel of crude oil at a certain time in the future.

If spot prices are expected to be higher in the future, then the current futures price will be higher than the spot price. If spot prices are expected to be lower in the future, then the futures price will likely be lower than the spot price.

An investor in futures earns a risk premium which is the difference between current futures price and the expected future spot price.

A Portfolio Of Commodities

Gorton and Rouwenhorst suggest that investors can earn returns that are of a similar level to that of equities if they invest in an equal weighted portfolio of commodity futures contracts over a long period of time.

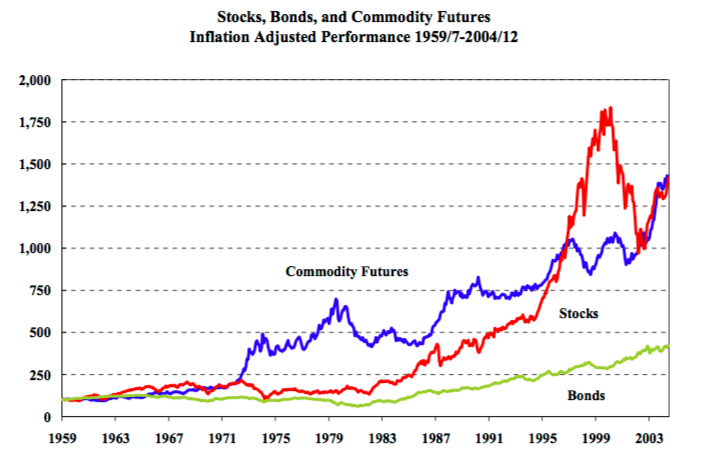

To show this, the authors constructed an equal weighted portfolio of common and liquid commodity futures, from 1959-2004 and tested it against the S&P 500.

Their portfolio was created by calculating the total monthly returns from various commodity futures and dividing by the number of different commodity futures that were present at that point in time and applying that weighting to each commodity. The portfolio was then effectively rebalanced monthly based on overall returns.

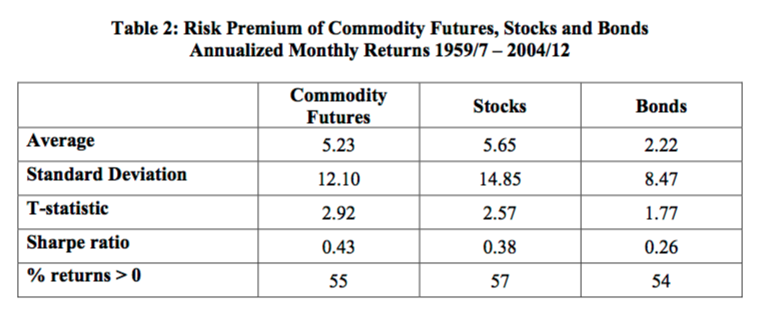

The portfolio of futures contracts ended up with returns very similar to those generated by equities. Over the testing period, the equal weighted portfolio of commodity futures returned 0.89% per month versus 0.93% for the S&P 500.

Most interestingly, the equal weighted portfolio of commodity futures had a lower standard deviation and higher Sharpe ratio compared to equities. Both of the asset classes outperformed corporate bonds.

Negative Correlation

Another interesting element of this study is the way in which commodity futures returns had a negative correlation to equities. Gorton and Rouwenhorst suggest that because of this negative correlation, commodity futures could potentially be used as a hedge for equities in an investor’s portfolio.

Commodities therefore have the potential to improve diversification, smooth an investors drawdowns and produce a more comfortable ride.

While not all investors will have the capital base to trade outright in commodity futures contracts, investors can certainly take advantage of commodity ETNs (exchange traded products) like DJP (the iPath Bloomberg Commodity ETN).

Updated Study

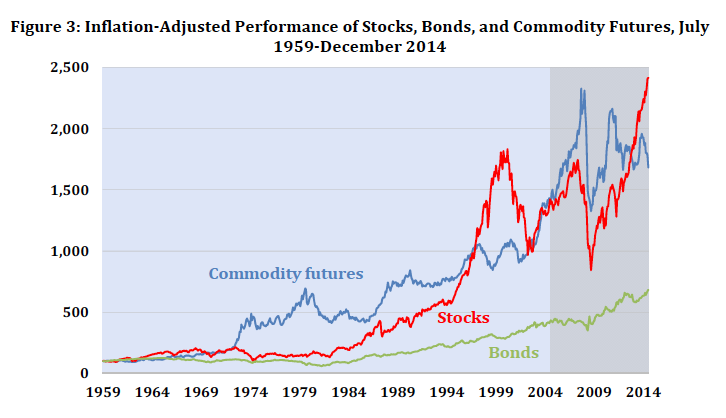

It’s worth noting that Gorton and Rouwenhorst produced an updated study to this in 2015, thus giving the authors ten years of out of sample data to evaluate their research.

As expected, the overall returns for commodities during this time were much lower owing to the poor performance we have witnessed since 2008.

However, the key insights from the original study were largely verified in the out-of-sample results. That is, commodity futures provided a return that was significant, superior to bonds and less correlated to the performance in equities and bonds.

The chart below shows how the three asset classes of stocks, bonds and commodity futures have fared since 1959. The grey shaded area represents the period since the original study:

Key Takeaway For Investors

The key takeaway for investors is that commodity futures are worthy of investigation as a long term investment vehicle.

While overall returns are comparable to equities in the long term, they are able to achieve those results with lower levels of variance and with a superior Sharpe ratio.

Thus, including commodities in a portfolio can improve diversification and lead to better risk-adjusted returns overall.

Contrary to popular wisdom, the results suggest that not only are the returns of commodity futures strong, they are also potentially a safer investment than equities.

At the current time, investor attention seems to be predominantly focussed on equities. But there will come a time when commodities have their time in the sun once again.

Joe

whats the best way for equities investors to invest in commodities,just trend following using a watchlist composed of a basket of ETFs? Should typical stock trend following approaches apply or how should they be adjusted to suit? Some commodities aren’t very volatile, so should they be levered up somehow or ignored?

Trend following is a definite possibility but I haven’t looked into it closely. I would look at ETFs that carry equal weighted futures and rebalance regularly like in the papr. The paper includes 36 different commodities.

I am looking at ETFs like GDG, DJP but maybe some other readers will have some suggestions.

Thanks for sharing Joe! I agree that most investors are probably unaware of commodity investing. But to your point adding this asset class to the portfolio can really smooth out returns overall. Thanks again!