I recently stumbled across an interesting article on the website medium.com which showed some incredible backtest results for a parabolic stock trading system.

The strategy attempts to find explosive, profitable stock trades and was shown to produce a 397.55% net return between 1st January and 12th November 2017.

The system was backtested in Amibroker so I thought I would code the strategy up and compare results.

Parabolic Trading System Rules

The strategy uses technical rules to pick stocks. From what I can tell, the rules of this strategy are as follows:

Buy Rules

- RSI(30) > 70

- Weekly RSI(30) > 70

- Weekly RSI(30) > Daily RSI(30)

- MA(10) > MA(20) > MA(50) > MA(100)

- Close > MA(10)

Sell Rules

- Close is > 2% below MA(10)

- OR 8% fixed stop loss

Position Sizing & Ranking

- 50% position size, maximum of two positions, no leverage

- Ranking is difference between Weekly RSI(30) and daily RSI(30), greatest preferred first

Interpretation & Results

It’s clear the point of this strategy is to find strongly trending stocks using technical indicators.

RSI is used to find stocks that are in a strong overbought phase and a series of moving averages are used as confirmation.

The idea is to jump on a strong trend and then exit as the trend begins to change. Little diversification is used with capital split between just two positions.

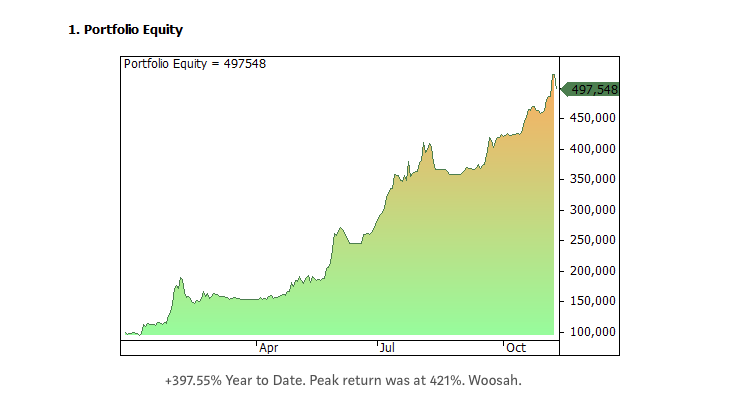

The author of the article applies the strategy to a selection of stocks from the Phillipines and records a net profit of 397.55% from 17 trades with a win rate of 71% and a maximum drawdown of -22.58%.

Below you can see the rather nice looking equity curve from this strategy:

Testing The System On US Micro Cap Stocks

The performance of this strategy seems a little too good to be true but let’s see how it gets on in another test.

The idea of the strategy is to find fast moving stocks so I didn’t think it would be fair to test this strategy on well known US stocks. So I decided to run the strategy on US micro cap stocks instead.

I therefore used the Russell Micro Cap Universe provided by Norgate data. This database is adjusted for dividends, corporate actions and is supposedly clean of survivorship bias.

I included commissions of $0.01 per share and set execution to the next day open for all trade entries and exits.

The following equity curve shows results of the strategy when applied to the US micro cap database between 1st January 2017 and 1st December 2017:

Below you will see a selection of trade results from the backtest. For example, a 76.59% gain in PLSE and a -10.08% loss in ALT:

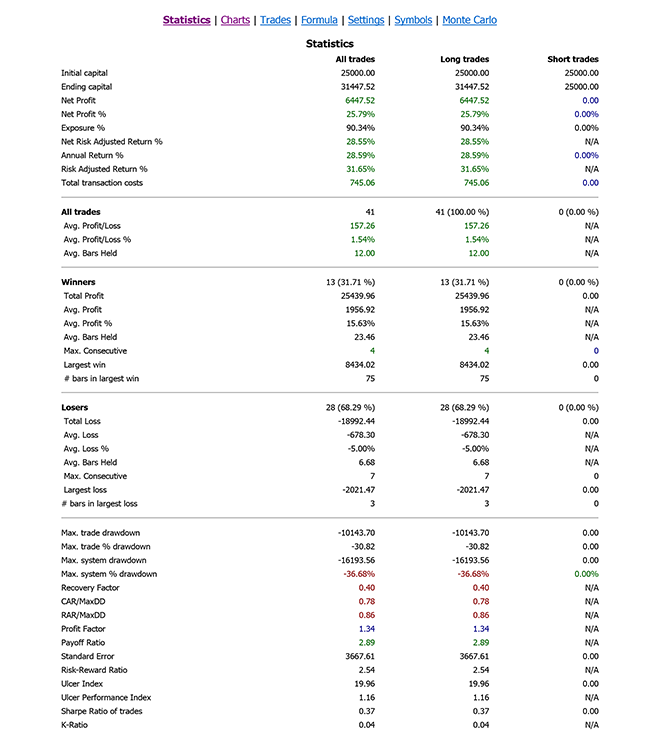

Following are some more detailed stats of the system output from Amibroker:

You can see that we have recorded a net profit of 25.79% on US micro caps. Not actually a bad result but it is nowhere near as good as the 400% we were hoping for.

You can also see that we are underperforming on a number of metrics. Noticeably, our maximum drawdown is -36.68% and our win rate is only 31.71%.

This gives a Sharpe of 0.37. Our Payoff Ratio is quite good, however, at 2.89.

Longer Timeframe Test

Although 26% return is not as good as 400%, it is still pretty good so let’s see how the strategy holds up when testing on a longer timeframe.

The following equity curve, therefore, shows results for the same system between 1/2010 to 1/2017:

As you can see, when extending this strategy out to a longer data period, results have declined significantly and this is now a losing system according to our analysis.

The annualised return is now -15.39% with a maximum drawdown of -75% and a win rate of 33.33%.

So What Is Going On?

We have taken a profitable trading strategy found online and applied it to a universe of US micro cap stocks and we have been disappointed in the results.

There could be numerous reasons to explain this. For instance:

- The strategy might be a curve fit strategy with little chance of working on other data periods or markets.

- The original results might not be accurate due to a backtesting error such as lack of commissions, existence of survivorship bias, inaccurate data or future leak.

- The original strategy simply might not work well on our database of US equities.

- We have made a mistake somewhere and our results are not realistic.

Considering these results, it seems highly likely that the strategy is curve fit to the original data. There is also the possibility of inaccuracies/biases in the data.

However, we also can’t rule out the fact that this strategy just might not work well on the market we tested. Maybe this system actually does work very well on the Phillipines stock market!

If you would like to find out for yourself, I have put together some Amibroker code here. Try it out for yourself on the markets of your choice.

A tip: try adjusting RSIRule3 and removing the fixed 8% stop loss.

Simulations and charts from Amibroker using data from Norgate.

Thank you Joe for this beautiful article. I enjoy reading this. I appreciate your thoughts and ideas. Great job.