The stock market cannot go up forever. At some point there will be another stock market crash and as always there will be some winners and some losers.

In this article, I look at some techniques investors can use during a market crash and reveal two interesting strategies based on a recent academic paper.

Tactics For A Stock Market Crash

The biggest problem an investor has is first knowing whether or not a stock market crash is around the corner. Such events are inherently unpredictable and trying to time the market in and out (without any system in place) is usually a recipe for disaster.

Because of this, many stock investors will attempt to hedge their portfolios when they feel that the risk is heightened. Following are some typical ways investors might hedge their equity portfolios during times of market stress:

Short Selling Stocks – Short selling stock indices or individual stocks in order to profit from their fall and offset long equity positions.

Buying Put Options – Buying put options such as at-the-money puts on the S&P 500 to profit from an immediate fall.

Buying VIX Futures – Buying VIX futures or VIX ETFs that profit from a rise in market volatility.

Buying Bonds – Holding safe haven assets such as Treasury bonds which typically rise when stock markets fall.

Buying Gold – Holding safe haven assets such as gold which typically rise during market crisis.

Utilising Short-Term Systems – Using short-term systems that are designed for high volatility markets.*

Day Trading – Engaging in day trading methods to profit from volatility both long or short during a stock market crash. This is a high risk strategy but has the advantage of no directional bias.

The Best Strategies For The Worst Crises

The strategies shown above all have advantages and disadvantages and are not suitable all of the time or for all investors. The most appropriate method is investigated further by recent research from Cook et al. in a paper called The Best Strategies For The Worst Crises.

This paper sheds some light on some of the methods mentioned above. Furthermore, it suggests that:

- Holding and continuously rolling S&P 500 put options is a reliable strategy for a sudden market fall but too costly to be the optimal strategy.

- Holding safe-haven Treasury bonds is an unreliable hedge due to the post-2000 negative bond-equity correlation – a historical rarity brought on by recent central bank monetary policy.

- Long gold and long credit protection portfolios sit somewhere ‘between puts and bonds in terms of cost and reliability’.

After describing these methods, the paper goes on to consider a number of different tactics for protecting capital during a stock market crash and concludes that two specific strategies come out on top; trend following futures (described in the paper as futures time-series momentum) and long-short equity based on stock quality measures.

Trend Following Futures

The ‘futures time-series momentum’ strategy shown in the paper is based on a strategy that takes long and short momentum positions in a diversified basket of different futures contracts and is shown to perform well during every one of the seven most severe stock market crashes since 1985.

The exact strategy uses simple 1, 3, and 12-month momentum scores to capture short, medium and long-term trends, the result of which is divided by the standard deviation of returns to calculate a risk-adjusted position size.

A gearing factor is chosen to target 10% annualised volatility and risk is spread across six different groups: 25% currencies, 25% equity indices, 25% fixed income, and 8.3% to each of agricultural products, energies, and metals.

In addition, the equity part is capped so as to only allow short equity positions and no longs. This is because we will in theory have enough equity exposure already.

Although it may sound complex, this in fact quite a typical trend following type strategy and similar to those utilised by many in the managed fund space.

Findings

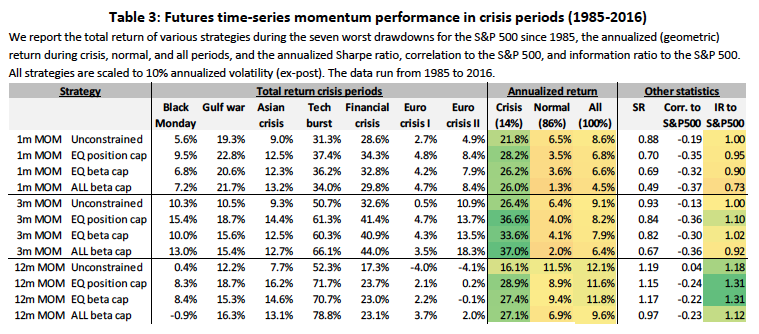

The following table shows some results of the futures momentum strategy during different market crises:

You can see, for example, that a 1-month momentum strategy produced an annualised return of 21.8% across seven recent market crises including a 31.3% return during the dot-com crash.

Although several variations are shown, they are all similar in performance and the results indicate that trend following futures is a profitable strategy during stock market downturns.

This is quite a typical trend following system for trading futures and it’s strong performance during market crises seems to make economic sense. Most of us will recall how well trend following funds did in the 2008 crisis as a memorable example.

Long-Short Equity Based On Quality Factors

A long-short equity strategy based on quality factors is the other recommended strategy shown in the paper.

It consists of shorting the lowest quality stocks during a market crisis and going long on the highest quality stocks. Since ‘quality’ is quite a subjective term a number of different quality measures have been considered.

The different quality measures are devised based on simple formulas which act as a ranking measure for a universe of mid and large cap US stocks. The portfolio then goes long the highest ranked stocks and short the lowest ranked stocks.

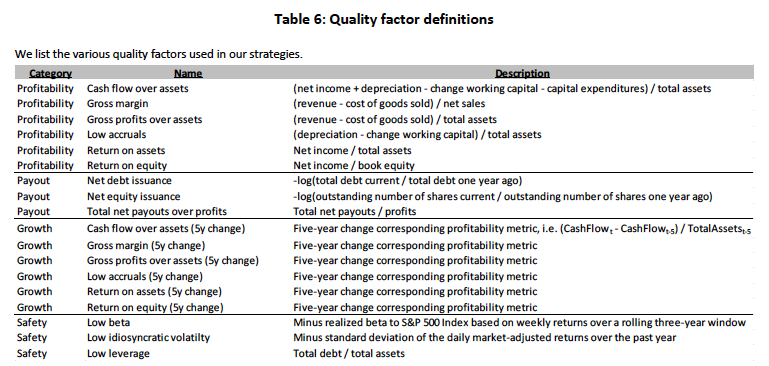

The table below shows the calculations for each of the quality factors analysed:

For example, the return on equity quality factor is calculated by dividing net income by book equity. At each date, the raw signal value is ranked and a cross-sectional analysis is also undertaken to prevent the impact of outliers.

Findings

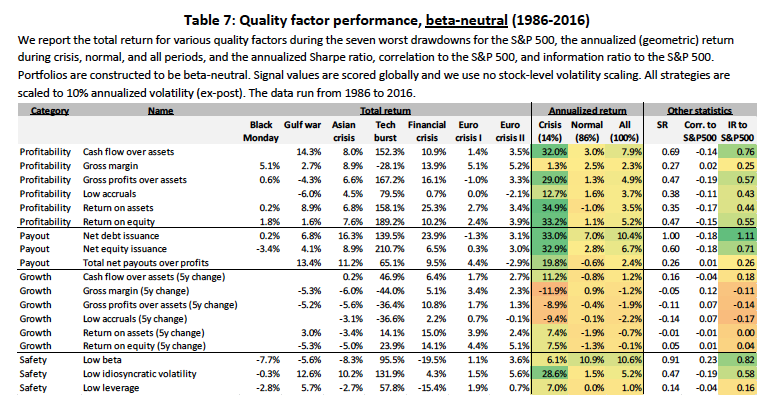

The next table shows the results for some of the different quality factors shown in the paper:

You can see that for most factors, the annualised return is higher during the crisis period than the return during normal periods. According to the authors this suggests a ‘crisis-hedge property’ and is most prevalent in the categories of profitability and payout.

The net debt issuance factor is arguably the strongest performer showing a 33% annualised return in crisis periods and a 10.4% annualised return overall. This scores a Sharpe ratio of 1.00.

The calculation for this net debt issuance factor is shown as:

net debt issuance = -log(total debt current / total debt one year ago)

A simplistic way to interpret this factor is to go long companies with improving debt situations (relative to peers) and go short companies with deteriorating debt situations.

Overall, the paper reveals that a long-short strategy of shorting low quality stocks and going long high-quality stocks performs well in a stock market crash and that this can be explained by a ‘flight to quality effect’.

This also seems to make economic sense. We can surely recall times in the past where investors have shed risky debt-fuelled growth stocks and flocked to defensive, more cash-rich companies in times of crisis.

Putting It Together

To conclude their paper, the authors look at the correlation between the two strategies and find that the correlation is small enough for there to be additional benefits of combining the two strategies together.

Thus, they form a composite strategy which is then back-tested at different allocation weights in order to judge the overall performance.

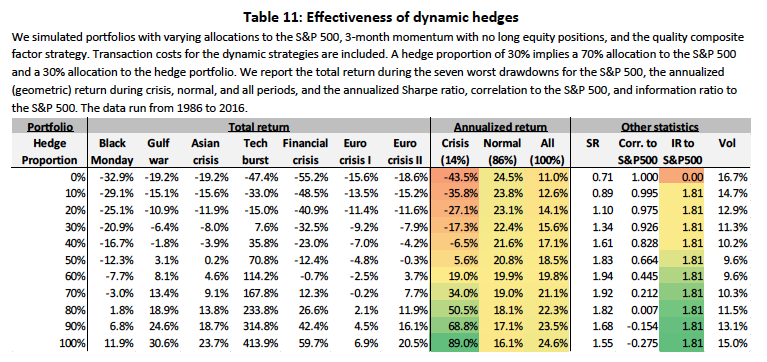

The authors allocate a proportion of assets to the combined hedge portfolio (trend following and long-short equity) and the remaining assets go to the S&P 500.

A hedge proportion of 30% implies a 70% allocation to the S&P 500 and a 30% allocation to the hedged portfolio. While a hedge proportion of 90% implies a 10% allocation to the S&P 500 and a 90% allocation to the hedged portfolio.

Statistics for the portfolios are shown below:

You can see that the largest annual return actually came from a 100% allocation to the hedged portfolio which produced an annualised return of 24.6% between 1986 and 2016.

However, the best Sharpe ratio (1.94) was achieved with a 60% allocation to the hedged portfolio and a 40% allocation to the S&P 500.

Conclusion

In this article we looked at some ways to protect capital during a stock market crash and revealed two strategies that do well based on the findings of a recent financial paper. Those strategies were shown to be trend following futures and long-short equity based on quality factors.

Allocating 60% of capital to the hedged portfolio with 40% to the S&P 500 was shown to return over 20% annually with a high Sharpe ratio – based on simulations between 1986 to 2016. Furthermore, the strategy seems logical and based on economic sense.

Such a strategy may be complex for ordinary investors, however. Trend following and short selling are quite sophisticated techniques and many investors could end up making mistakes in the construction of portfolios and following the strategy rules.

Perhaps simpler alternatives could be possible through the use of ETFs. This could be the focus for another article. If you know any way to implement such a strategy more simply, please let us know in the comments.

* Stock market crashes can actually be quite profitable periods for trading systems and day traders since market efficiency goes out the window. A system that might do well in such an environment is in fact included in Marwood Research called Overnight Reversal. I am waiting to use it in the event of a market crash.

Sources

Cook, Michael and Hoyle, Edward and Sargaison, Matthew and Taylor, Dan and Van Hemert, Otto, The Best Strategies for the Worst Crises (June 15, 2017). Available at SSRN: https://ssrn.com/abstract=2986753